Empowering Consumers with AI-Driven Legal Defense

Master legal letters for debt collection with AI-driven defense. Spot FDCPA violations, respond to summonses, and protect your rights now.

The Evolution of Legal Defense Tech in Debt Collection

Receiving a debt collection letter can be a daunting experience. In May 2026, with consumer debt levels consistently high, understanding these legal communications is more critical than ever. We are here to transform that initial stress into an opportunity for empowered action.

Receiving a debt collection letter can be a daunting experience. In May 2026, with consumer debt levels consistently high, understanding these legal communications is more critical than ever. We are here to transform that initial stress into an opportunity for empowered action.

This comprehensive guide will demystify legal letters for debt collection. We’ll explore what these letters are, when they’re used, and the specific legal requirements they must meet under federal and state laws. You will learn about essential elements for effective letters, how to customize templates, and the different types of response letters consumers can send to protect their rights.

The landscape of debt defense is rapidly evolving. Innovative tools, such as those leveraging AI legal debt defense, now offer sophisticated support for consumers. We’ll also highlight common mistakes to avoid and outline the steps that follow if a letter does not resolve the debt. Our goal is to equip you with the knowledge to navigate these challenges confidently, safeguard your financial well-being, and improve collection outcomes while staying fully compliant.

The realm of debt collection, once dominated by manual processes and often opaque practices, is undergoing a profound transformation thanks to legal defense technology. In May 2026, artificial intelligence (AI) and automation are not just buzzwords; they are becoming integral to ensuring FDCPA compliance and enhancing accessibility for consumers. This technological shift empowers individuals to proactively address debt collection efforts, detect potential violations, and even prepare for litigation with unprecedented ease.

The Fair Debt Collection Practices Act (FDCPA) remains the cornerstone of consumer protection against abusive debt collection practices. However, interpreting its nuances and applying them effectively has historically been challenging for the average consumer. Legal defense tech bridges this gap, offering automated screening of communications, sophisticated document assembly, and real-time guidance. This allows consumers to understand their rights and respond strategically, shifting the balance of power. Regulatory bodies are also adapting, with an increasing focus on how technology can both aid and potentially complicate compliance, leading to ongoing shifts in best practices for both collectors and consumers.

Scaling Access Through Legal Defense Tech

Machine learning algorithms are revolutionizing how consumers interact with the legal system regarding debt. These systems can analyze vast amounts of data, identifying patterns and potential FDCPA violations that might otherwise go unnoticed. Document assembly tools, powered by AI, allow individuals to generate tailored debt validation letters, cease and desist requests, and even dispute letters with minimal effort. This significantly lowers the barrier to entry for effective debt defense, moving beyond generic templates to highly personalized and legally sound communications.

For instance, tools can help consumers draft letters to dispute debts they don’t believe they owe, or to request more information, much like the sample letters provided by the CFPB. These platforms can guide users through the process of asserting their rights, ensuring that critical information is included and that the communication adheres to federal guidelines. This empowerment is particularly vital for those who might not have access to traditional legal counsel, offering a robust self-help resource. The trend in May 2026 is towards more intuitive interfaces and comprehensive support, making sophisticated legal strategies accessible to anyone with an internet connection.

Identifying FDCPA Violations with Legal Defense Tech

One of the most powerful applications of legal defense tech is its ability to help consumers identify and document FDCPA violations. The FDCPA provides for statutory damages of up to $1,000 per lawsuit, plus attorney fees, for violations. However, proving these violations often requires meticulous record-keeping and a deep understanding of the law. AI-driven platforms can analyze communication logs—whether calls, emails, or letters—to flag instances of harassment, misrepresentation, or improper contact times.

For example, if a debt collector contacts a consumer outside of the permissible hours (typically 8 AM to 9 PM local time), or continues contact after a written cease and desist request, these tools can help document the violation, laying the groundwork for potential legal action. Some platforms even offer automated screening of incoming collection letters, checking for the required Mini-Miranda warning or the 30-day validation notice. This proactive approach not only helps consumers protect their rights but also creates a deterrent for collectors who might otherwise engage in non-compliant practices. The ability to quickly identify and act on these violations can be a game-changer, potentially leading to debt erasure or financial compensation for the consumer.

Navigating the Anatomy of Legal Letters for Debt Collection

Legal letters for debt collection serve as formal communications, typically from a creditor or a third-party debt collector, demanding payment for an outstanding debt. Understanding their anatomy is crucial for both those sending and receiving them. These letters are not merely requests for payment; they are structured legal documents designed to achieve specific objectives, often serving as a precursor to more aggressive collection tactics or even litigation.

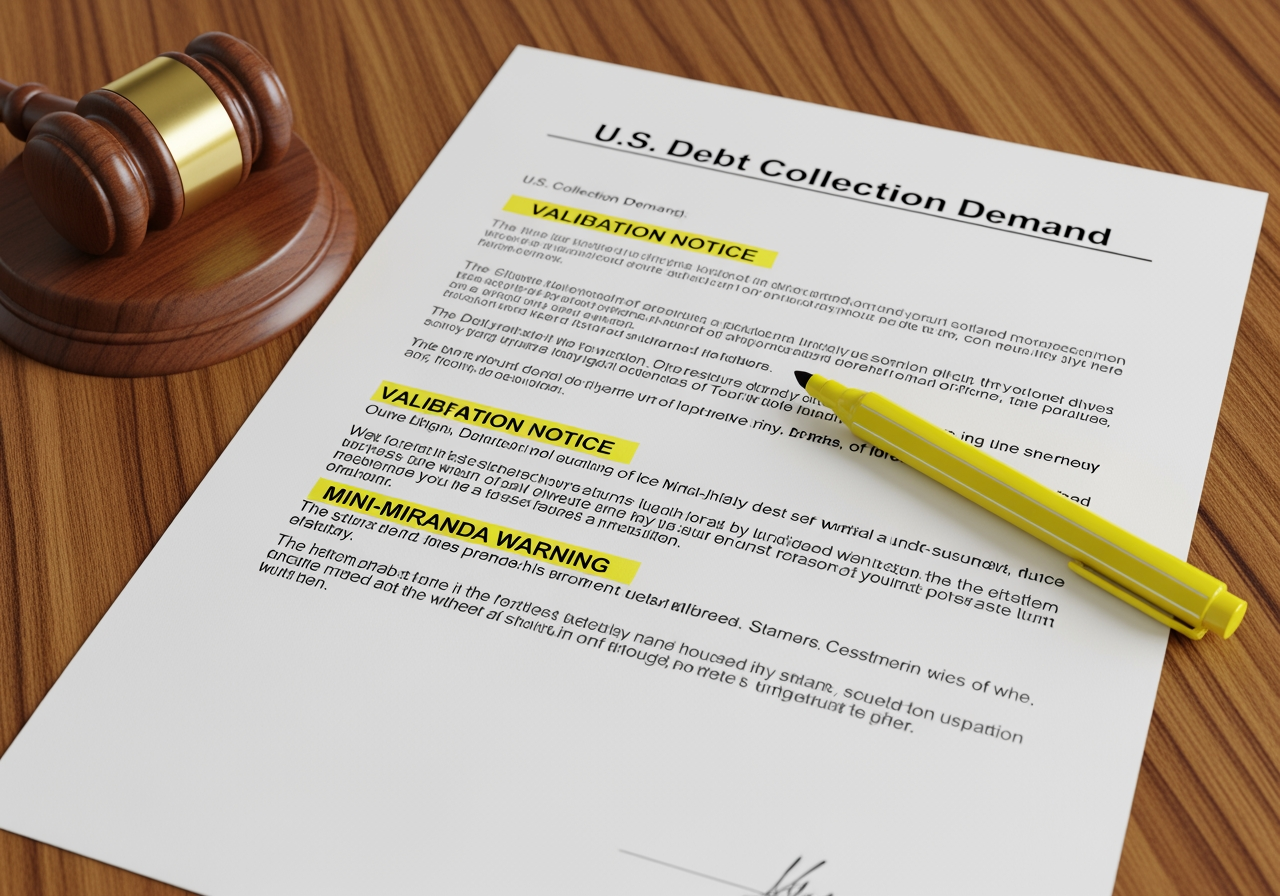

A fundamental component of any compliant debt collection letter, particularly from a third-party collector, is the validation notice. This notice, mandated by FDCPA Section 1692g(a), must inform the consumer of their right to dispute the debt within 30 days of receiving the letter. During this 30-day window, the collector must cease collection efforts if the debt is disputed in writing, until verification is provided. The notice should clearly state the amount of the debt, the name of the creditor to whom the debt is owed, and a statement that if the consumer disputes the debt in writing within 30 days, the collector will obtain verification of the debt.

Another critical element is the Mini-Miranda warning, which states that the communication is from a debt collector attempting to collect a debt and that any information obtained will be used for that purpose. This disclosure is a cornerstone of FDCPA compliance, ensuring transparency about the nature of the communication.

Effective collection letters also include clear creditor identification, specifying who the original creditor was and who currently owns the debt. They detail the principal balance owed, any accrued interest, and applicable fees. For businesses collecting their own debts, such as attorneys chasing unpaid invoices, the letter will reference the original contract or agreement and provide a chronological context of the overdue payments. For example, a law firm might send a letter to a client for outstanding fees, detailing the services rendered and the amount due, similar to how attorneys pursue unpaid hours, which average 9% of invoiced time, according to industry statistics.

When drafting a collection letter, whether it’s a first attempt to collect a debt or a more serious legal proceedings letter, clarity and professionalism are paramount. Templates from resources like LegalZoom or Rocket Lawyer offer structured formats for various stages of collection, from amicable reminders to final demands. These often include specific sections for the amount owed, the due date, late fees, payment instructions, and the consequences of non-payment. For instance, a Minnesota demand for payment letter might outline the specific terms of a payment agreement and warn of legal action if the debt remains unpaid. Similarly, a Texas-specific debt collection letter template will ensure compliance with both federal FDCPA and the Texas Debt Collection Act, including state-required disclosures.

Feature Debt Validation Letter (Consumer Sends) Cease and Desist Letter (Consumer Sends) Purpose Demands proof that the debt is legitimate, accurate, and belongs to the consumer; halts collection until verified. Commands a debt collector to stop all communication (or limit it to specific methods/times) regarding a debt. Legal Basis FDCPA §809(b) – Consumer’s right to dispute and request verification within 30 days of initial contact. FDCPA §805(c) – Consumer’s right to stop communication. Effect Collector must stop collection until verification is mailed. If they can’t verify, they must cease collection and report the debt as disputed. Collector must cease communication, except to notify of legal action or that collection efforts are being terminated. Debt is not erased. Timing Most powerful if sent within 30 days of initial contact, but can be sent anytime. Can be sent anytime communication is unwanted. Key Information Consumer’s name, collector’s name, account number, request for specific verification documents (original contract, payment history, etc.). Consumer’s name, collector’s name, account number, clear statement to cease contact (or specify contact methods). Outcome Can lead to debt being dropped, verified, or reported as disputed. Stops harassment, but collector can still sue or report to credit bureaus. When a consumer receives such a letter, especially one that hints at legal proceedings, it’s crucial to understand their rights. The letter itself does not automatically grant the collector the right to sue or take specific action; it’s often a warning. However, ignoring it can lead to escalation. For those struggling with debt collectors, understanding the contents of these letters and knowing how to respond is the first step towards effective defense.

Strategic Responses to Urgent Collection Threats

When a debt collection letter escalates beyond mere demands and begins to threaten legal action, consumers must shift to a more strategic and urgent response. Ignoring these threats can lead to severe consequences, including wage garnishment, bank levies, and default judgments, which can significantly impact financial stability. Proactive defense is key to protecting your assets.

If you receive a summons or notice of a lawsuit, your immediate priority is to understand what to do when sued by a debt collector: complete first steps guide. The most critical step is to respond within the specified deadline. Failing to do so almost always results in a default judgment against you, granting the collector the legal right to pursue aggressive post-judgment remedies without further court proceedings. This is where the importance of understanding filing deadlines becomes paramount.

One effective strategy is to file a robust answer to the lawsuit. This answer should not only deny the debt but also raise any available affirmative defenses. These are legal arguments that, if proven, can defeat the collector’s claim, even if the debt itself is valid. Examples include the statute of limitations, identity theft, or improper service of the lawsuit. Furthermore, filing a counter-affidavit can be a powerful tool. A strong counter-affidavit can challenge the collector’s evidence and force them to prove every aspect of their claim. For guidance on this, consider resources like key to strong answer in a collection lawsuit: solid counter-affidavit and filing a counter-affidavit when answering a debt collection lawsuit.

Protecting your assets is another critical concern. Understanding can debt collectors take my wages and bank account? is vital. Many states have laws protecting certain types of income (like Social Security benefits or disability payments) and assets from collection. Knowing what constitutes “exempt property” can help you safeguard your finances.

Beyond litigation, negotiation can also be a strategic response. If a debt is legitimate but you cannot pay the full amount, a debt settlement letter can be sent to collection agencies to propose a lower payoff. This approach can be particularly effective if the debt is old or if the collector purchased it for a fraction of its original value, as they often do. Resources like SoloSuit’s sample letter to collection agencies to settle debt can provide a starting point for these negotiations.

For those simply seeking to stop harassing calls and letters, a cease and desist letter can be highly effective. While it won’t erase the debt or prevent a lawsuit, it legally compels collectors to stop contacting you, with limited exceptions. SoloSuit also offers templates for cease and desist letters to debt collectors. However, stopping contact does not stop the debt itself, and legal action remains a possibility.

Navigating these urgent threats requires informed action. Whether it’s responding to a lawsuit, negotiating a settlement, or simply managing communication, understanding your options and acting decisively can make all the difference. For those wondering do I need a lawyer for a debt collection lawsuit?, it’s often advisable to seek legal counsel, especially when facing litigation, to ensure the best possible defense.

Essential Elements in a Lawsuit Answer:

- Case Information: Court name, case number, plaintiff, defendant.

- General Denial: A statement denying all allegations in the complaint.

- Specific Denials/Admissions: Address each specific allegation, admitting what is true, denying what is false, and stating lack of knowledge for others.

- Affirmative Defenses: Legal arguments that, if proven, defeat the plaintiff’s claim (e.g., statute of limitations, lack of standing, payment, identity theft, improper service, FDCPA violations).

- Counterclaims (Optional): Claims you might have against the plaintiff (e.g., FDCPA violations).

- Demand for Proof: Request that the plaintiff prove all elements of their case.

- Signature: Your signature and contact information.

- Certificate of Service: Proof that you sent a copy of your answer to the plaintiff’s attorney.

State-Specific Nuances and Federal Protections

While the FDCPA provides a baseline of federal protection for consumers, state laws often add layers of complexity and additional rights. Understanding these state-specific nuances is crucial for both collectors ensuring compliance and consumers mounting an effective defense. What might be permissible in one state could be a violation in another, making jurisdictional compliance a significant factor.

For instance, states like Texas have their own debt collection acts that supplement the FDCPA. A Texas debt collection letter must not only adhere to federal FDCPA requirements, including the validation notice and Mini-Miranda, but also often include specific state-mandated disclosures as attachments. The Texas State Law Library provides a wealth of free resources and forms for responding to lawsuits and asserting consumer rights, including forms for exempt property. This highlights the importance of checking local resources when dealing with debt claims.

In Illinois, consumers can leverage tools like the Illinois Legal Aid Online’s Easy Form generator to create personalized letters to debt collectors. This tool helps consumers assert their collection-proof status, notifying collectors that their income and belongings are exempt from collection under state law. This protection is vital for low-income individuals or those receiving public benefits, as certain assets cannot be seized by private creditors.

Georgia also offers specific guidance on using FDCPA letters through organizations like Georgia Legal Aid. These resources often provide step-by-step instructions for sending debt verification and cease communication letters, tailored to local legal aid practices. This ensures that even without an attorney, consumers can effectively assert their rights and report violations to appropriate bodies like the FTC or state Attorney General.

Michigan, too, has its own set of rules and resources. While the FDCPA is federal, Michigan’s court rules and collection practices can influence how debt collection lawsuits proceed and what types of notices are issued. Resources like Michigan Debt Collection Lawyers offer free credit dispute letters and validation letters, reflecting the state’s specific legal environment. The State of Michigan also provides information on various types of letters and notices related to taxes and other debts.

Statutes of limitations are another critical state-specific factor. These laws set a time limit within which a creditor or collector can sue to collect a debt. These limits vary significantly by state and type of debt, often ranging from 2 to 10 years. If a debt is “time-barred,” a collector cannot legally sue to collect it, although they may still attempt to collect through other means. Knowing your state’s statute of limitations can be a powerful defense.

The rise of electronic filing in courts across the country also impacts how consumers respond to lawsuits. While some states offer online tools for filing answers, others may require traditional paper filings. Understanding these procedural differences is crucial to avoid missing deadlines and inadvertently losing a case.

For those facing debt collection, remember that while federal laws like the FDCPA provide a broad shield, state laws often provide additional layers of protection or specific procedural requirements. Always consult state-specific resources or legal counsel to ensure full jurisdictional compliance and the most effective defense. For more general insights into the role of debt collectors and your rights, consider exploring resources like what is a debt collector under the FDCPA? your rights explained and struggling with debt collectors.

State-Specific Defense Resources:

- Texas: Texas State Law Library for forms and guides on debt claims and exempt property.

- Illinois: Illinois Legal Aid Online for Easy Forms to respond to debt collectors and assert collection-proof status.

- Georgia: Georgia Legal Aid for FDCPA letter templates and guidance.

- Michigan: Michigan Debt Collection Lawyers for free dispute and validation letters.

- General: State Attorney General’s office websites often provide consumer protection information and complaint forms relevant to debt collection.

Frequently Asked Questions about Debt Defense

What should I do immediately after receiving a court summons?

Receiving a court summons for a debt is a serious matter that demands immediate attention. Your first step should be to verify the deadline for your response, which is usually clearly stated on the summons. This deadline is critical, as missing it can result in a default judgment against you. Next, avoid admitting the debt to the collector or in any informal communication. Your formal response should be a carefully prepared legal document. You’ll need to draft a formal answer to the complaint, addressing each allegation made by the plaintiff. This answer is your opportunity to deny the debt, raise affirmative defenses, and potentially file counterclaims. Once drafted, you must file it with the local clerk of court and ensure you serve the plaintiff’s attorney with a copy, usually by mail. For a comprehensive guide on this process, refer to what to do when sued by a debt collector: complete first steps guide. If you’re unsure about the process, it’s wise to consider do I need a lawyer for a debt collection lawsuit?. Understanding who is suing me? original creditor vs. debt buyer explained can also inform your defense strategy, as debt buyers often have less documentation than original creditors. This is especially relevant given why debt collectors buy old debts.

Can a debt collector seize my bank account without notice?

Generally, no. A debt collector cannot directly seize your bank account or garnish your wages without first obtaining a court judgment against you. This process involves filing a lawsuit, serving you with a summons, and winning the case. If they win, the court issues a judgment, which is a legal declaration that you owe the debt. Only then can the collector seek a writ of execution from the court, which is a legal order allowing them to pursue post-judgment remedies like wage garnishment or a bank levy. Even with a judgment, there are often protections for certain funds. Many states have laws exempting specific types of income (like Social Security, disability, or unemployment benefits) and a certain amount of money in bank accounts from garnishment. This is part of your due process rights, ensuring you have notice and an opportunity to defend yourself before such drastic actions are taken. If you are concerned about this, understanding can debt collectors take my wages and bank account? is crucial.

How does a validation letter stop collection activity?

A debt validation letter is a powerful tool under the FDCPA. When you send a written request for validation within 30 days of receiving the initial communication from a debt collector, FDCPA Section 809 mandates that the collector must cease all collection activity until they provide you with verification of the debt. This means they cannot call you, send you letters, or report the debt to credit bureaus during this period. The verification they provide must include specific information, such as the amount of the debt, the name of the original creditor, and proof that you owe the debt. If they cannot provide adequate verification, they must stop collection efforts entirely. This effectively creates a reporting moratorium on the debt until proper validation is received. Even if you miss the 30-day window, sending a validation letter can still have sway, though the collector is not legally obligated to cease collection activities until validated. For detailed instructions on how to use this powerful defense, consult debt validation letters: your first line of defense against collectors. For more information on how credit card debt collection works, including how banks sell accounts, you can visit credit card debt collection: how banks sell your account.

Conclusion

In May 2026, the landscape of debt collection is more dynamic than ever, but so too are the tools available for consumers to protect themselves. From understanding the intricate legal requirements of debt collection letters to leveraging cutting-edge AI for proactive defense, individuals are increasingly empowered to navigate these challenges with confidence. The future of consumer law is moving towards greater equitable access to justice, where technology plays a pivotal role in demystifying complex legal processes and providing robust defense mechanisms.

By understanding your rights, recognizing the essential elements of legal letters, and strategically responding to collection threats, you can significantly improve your outcomes. Whether it’s through careful debt validation, assertive cease and desist requests, or a well-crafted lawsuit answer, informed action is your best defense. This shift towards tech-driven self-help contributes to greater systemic accountability within the debt collection industry, ensuring that collectors adhere to federal and state laws. As we look ahead, the integration of AI in legal defense promises to continue evolving, offering even more sophisticated and accessible tools to safeguard financial well-being for all.